Key takeaways

- Track every transaction under the correct rental property.

- Keep rental and personal finances clearly separated.

- Use consistent income and expense categories from month to month.

- Separate mortgage principal from interest, taxes, insurance, and escrow activity.

- Review records monthly instead of waiting until tax season.

On this page

- What Is Rental Property Bookkeeping?

- Why Rental Property Bookkeeping Matters

- What Landlords Should Track

- Keep Rental And Personal Finances Separate

- Organize Records By Property

- Build Consistent Income And Expense Categories

- Record Mortgage Payments Correctly

- Handle Security Deposits Separately

- Separate Repairs From Capital Improvements

- Keep Supporting Documents Outside PropioLedger

- A Practical Monthly Bookkeeping Workflow

- Reports Landlords Should Review

- Spreadsheet vs. Rental Bookkeeping Software

- Common Rental Bookkeeping Mistakes

- Example: One Month Of Bookkeeping

- Bookkeeping vs. Rental Property Accounting

- A Simpler Way To Organize Rental Property Finances

- Frequently Asked Questions

- Educational Disclaimer

What Is Rental Property Bookkeeping?

Rental property bookkeeping is the process of recording and organizing the income, expenses, balances, and financial activity associated with each rental property. A practical bookkeeping system helps landlords understand cash flow, compare property performance, maintain better records, and prepare more efficiently for tax season.

This guide is written for U.S. landlords and rental property owners with roughly 1 to 25 rental properties. The goal is not to turn you into a full-time accountant. The goal is to give you a repeatable system that keeps your rental property financial records clear enough to review during the year and useful enough to share with a tax professional when needed.

Why Rental Property Bookkeeping Matters

Bookkeeping matters because rental properties are not all the same. One property may produce steady income with low repair costs, while another may look profitable at the portfolio level but quietly consume cash through maintenance, vacancies, or unpaid balances.

Good landlord bookkeeping helps you understand actual cash flow, compare one property with another, identify unusually high costs, avoid missed or duplicated transactions, prepare cleaner information for a tax professional, and make better rent, repair, renovation, and portfolio decisions.

Tax preparation is one benefit, but it should not be the only reason you keep records. Monthly bookkeeping gives you an operating view of the rental business while there is still time to make decisions.

- See whether rent collected is actually covering operating costs and debt service.

- Spot properties with unusually high repairs, utilities, management fees, or turnover costs.

- Keep renter charges, payments, open balances, and past-due amounts visible.

- Avoid relying only on bank statements, which show cash movement but not property context.

- Create a cleaner handoff for accounting review and Schedule E preparation.

What Landlords Should Track

A good rental property bookkeeping system captures more than deposits and withdrawals. It should explain what happened, where it happened, who it involved, and how the transaction affects the property.

For small landlords, the most useful structure is usually property-level bookkeeping: every income item, expense, balance, and report should connect back to the correct rental property.

In more formal accounting systems, individual financial events may be documented as journal entries before becoming part of the general ledger. Landlords do not need to create those entries manually in every system, but the concept helps explain why transaction details and categories matter.

| Area | Examples | Why It Matters |

|---|---|---|

| Rental income | Rent, late fees, pet fees, parking, storage, reimbursements | Shows total property revenue |

| Operating expenses | Repairs, maintenance, insurance, utilities, supplies, management fees | Shows the cost of operating the property |

| Mortgage activity | Loan payments, mortgage interest, property taxes, insurance, escrow details from statements | Keeps debt service and escrow-related costs easier to review |

| Owner activity | Owner contributions, owner reimbursements, owner draws | Separates property performance from owner funding |

| Tenant balances | Charges, payments, credits, open balances, past-due balances | Helps landlords understand what is owed |

| Property-level results | Income, expenses, cash flow, profitability | Allows comparison across a rental portfolio |

Keep Rental And Personal Finances Separate

Mixing rental and personal spending is one of the fastest ways to make bookkeeping harder than it needs to be. Clear separation helps you review rental activity, explain transactions later, and avoid accidentally counting personal purchases as rental property expenses.

A dedicated rental bank account or credit card can simplify the process, but the right setup depends on your situation. The important bookkeeping principle is consistency: rental income, expenses, owner contributions, and owner distributions should be identifiable and separate from personal household activity.

If you cannot separate every account right away, use clear notes, categories, and property assignments so each transaction can be understood later.

Organize Records By Property

Property-level bookkeeping is central to understanding a rental portfolio. A combined total can tell you whether the portfolio made money, but it cannot tell you which property is performing well or which property is creating excessive costs.

For example, these two properties both contribute positive cash flow, but the second property has a much tighter margin. If you only look at portfolio totals, that difference is easy to miss.

| Property | Annual Income | Annual Expenses | Cash Flow |

|---|---|---|---|

| Oak Street Duplex | $39,600 | $17,800 | $21,800 |

| Maple Avenue Rental | $27,000 | $15,900 | $11,100 |

Build Consistent Income And Expense Categories

Consistent categories make reports useful. If you record a plumbing repair as Repairs one month, Maintenance the next month, and Miscellaneous later in the year, it becomes harder to understand what the property actually costs to operate.

Income categories often include rent, late fees, pet-related income, parking or storage income, tenant reimbursements, and other rental income. PropioLedger expense categories include loan payments, mortgage interest, property taxes, insurance, HOA fees, utilities, repairs, maintenance, improvements, supplies, yard service, cleaning service, and other property expenses.

The category names do not need to be complicated. They need to be consistent from month to month so reporting remains useful.

| Type | Common Categories |

|---|---|

| Income | Rent, late fees, pet-related income, parking, storage, tenant reimbursements, other rental income |

| Expenses | Loan payments, mortgage interest, property taxes, insurance, HOA fees, utilities, repairs, maintenance, improvements, supplies, yard service, cleaning service, other property expenses |

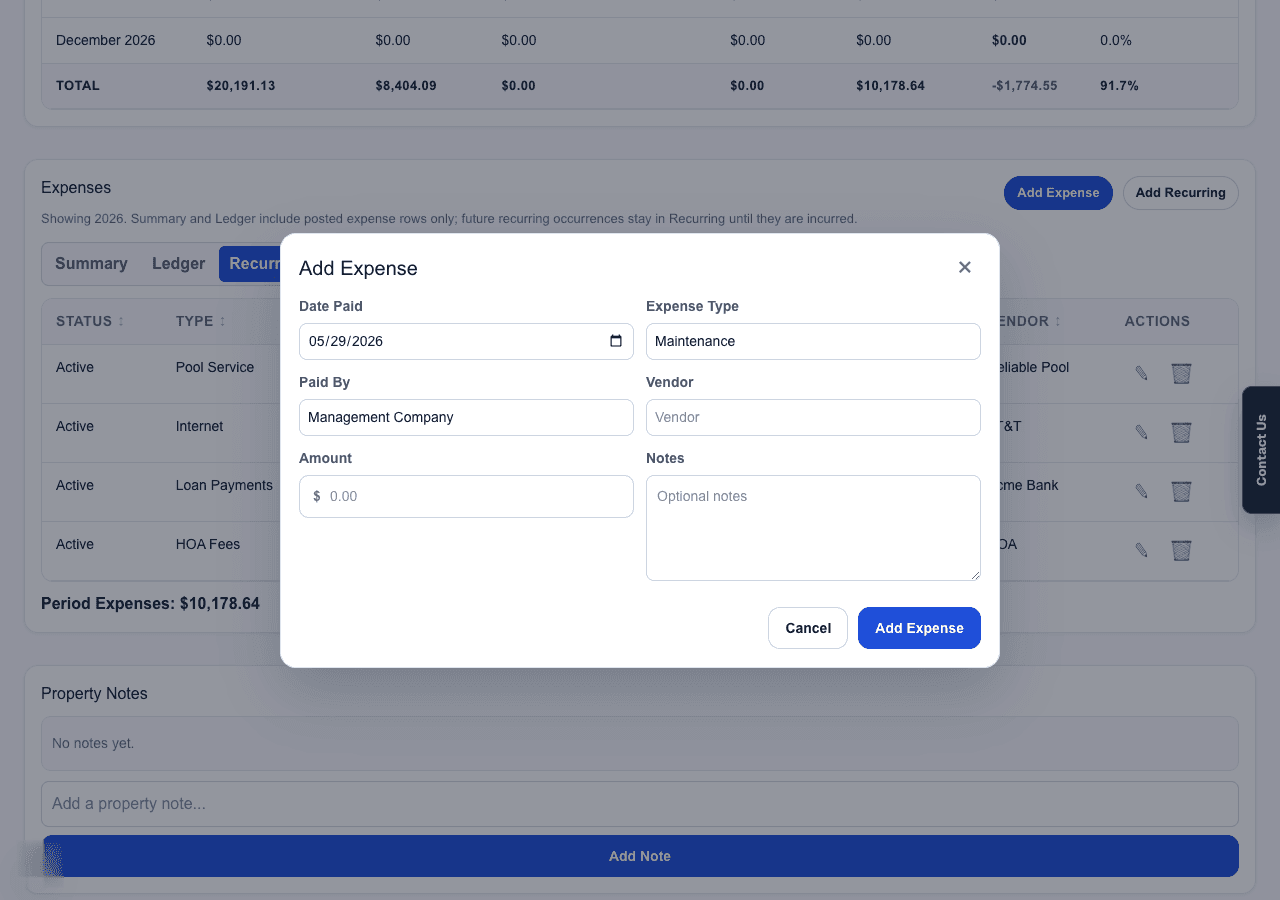

Record Mortgage Payments Correctly

Mortgage payments are easy to misclassify because one payment can contain several different components. A monthly loan payment may include principal and interest, and an escrow payment may later fund property taxes or insurance.

PropioLedger does not currently split a mortgage payment into principal, interest, taxes, and insurance automatically. In the application, landlords who want a simple cash-flow view can record the full debt-service outflow as Loan Payments. Landlords who want more detail can record known statement amounts using Mortgage Interest and Mortgage Principal, plus Property Taxes and Insurance when those amounts are paid separately or supported by escrow detail.

This keeps the app workflow accurate without implying that PropioLedger maintains a loan amortization schedule or automatically determines the principal and interest portions of each payment.

For financial review, the full loan payment matters for cash flow. For tax and accounting review, your professional may still need the underlying principal and interest detail from mortgage statements.

| Component | Example Amount | How To Track It |

|---|---|---|

| Full mortgage payment | $2,075 | Record as Loan Payments when tracking the full debt-service cash outflow |

| Interest portion | $1,425 | Record as Mortgage Interest when you are entering the interest amount from a statement |

| Property taxes paid separately or from escrow | $350 | Record as Property Taxes when you are recording that tax payment or escrow-supported tax detail |

| Insurance paid separately or from escrow | $175 | Record as Insurance when you are recording that insurance payment or escrow-supported insurance detail |

| Principal portion | $650 | Record as Mortgage Principal when you are entering the principal amount from a statement; it is excluded from operating-expense calculations |

Handle Security Deposits Separately

Refundable security deposits should not be treated like earned rent when received if the landlord expects to return them. They are funds held for a possible future obligation, not ordinary rental income in the same way monthly rent is.

State and local rules for security deposits can vary, including rules about handling, notices, deadlines, and bank accounts. Review the requirements that apply to your properties and speak with a qualified professional when needed.

In PropioLedger, security deposit payments are intentionally kept separate from rental revenue reporting. That distinction helps keep rental income cleaner while still giving landlords visibility into deposit-related balances.

Separate Repairs From Capital Improvements

Repairs and improvements can look similar in a checkbook, but they may be treated differently for tax and accounting purposes. A repair generally restores something to its existing condition. A capital improvement generally improves, replaces, or materially extends the useful life of the property.

The correct treatment depends on the facts. Significant projects should be reviewed with a qualified tax professional, especially when the work replaces a major system, improves the property, or is part of a larger renovation.

| Repair | Capital Improvement |

|---|---|

| Restores existing condition | Improves, replaces, or materially extends useful life |

| Fixing a leak | Replacing the entire plumbing system |

| Repairing part of a fence | Installing a new fence |

| Repairing an HVAC component | Installing a new HVAC system |

Keep Supporting Documents Outside PropioLedger

PropioLedger does not currently store receipt or invoice images. Landlords can keep supporting documents in a consistent external system such as Google Drive, OneDrive, Dropbox, or organized folders on a computer.

Use the same property names, dates, and vendor descriptions in both systems so documents can be matched to their corresponding transactions later. Within PropioLedger, each expense should contain enough context to understand the transaction later, including the property, date, amount, category, vendor when applicable, and notes.

A good note is short but specific. For example: Replaced leaking kitchen sink shutoff valve. That is more useful months later than simply writing repair.

A Practical Monthly Bookkeeping Workflow

Monthly review is where bookkeeping becomes useful. Waiting until year-end often means rebuilding the story from bank statements, receipts, emails, and memory. A monthly workflow keeps the records fresh while transactions are still easy to explain.

Use this checklist as a simple operating rhythm for bookkeeping for rental properties.

- Record rental income and other property income.

- Record and categorize expenses.

- Assign every transaction to the correct property.

- Review renter balances, payments, credits, and open charges.

- Verify mortgage components are recorded properly.

- Review unusual, missing, duplicate, or uncategorized transactions.

- Compare actual cash flow with expectations.

- Review reports for each property and for the portfolio.

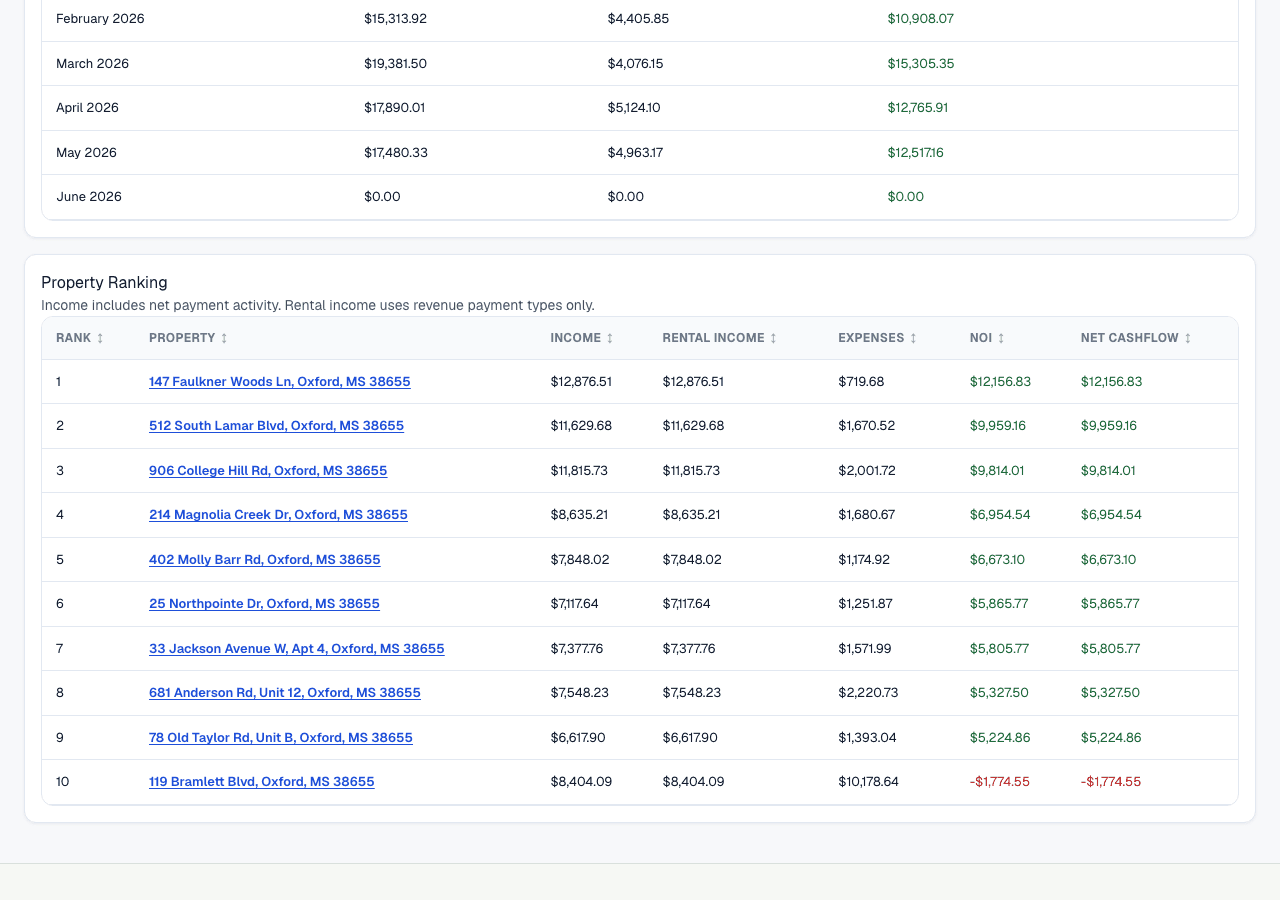

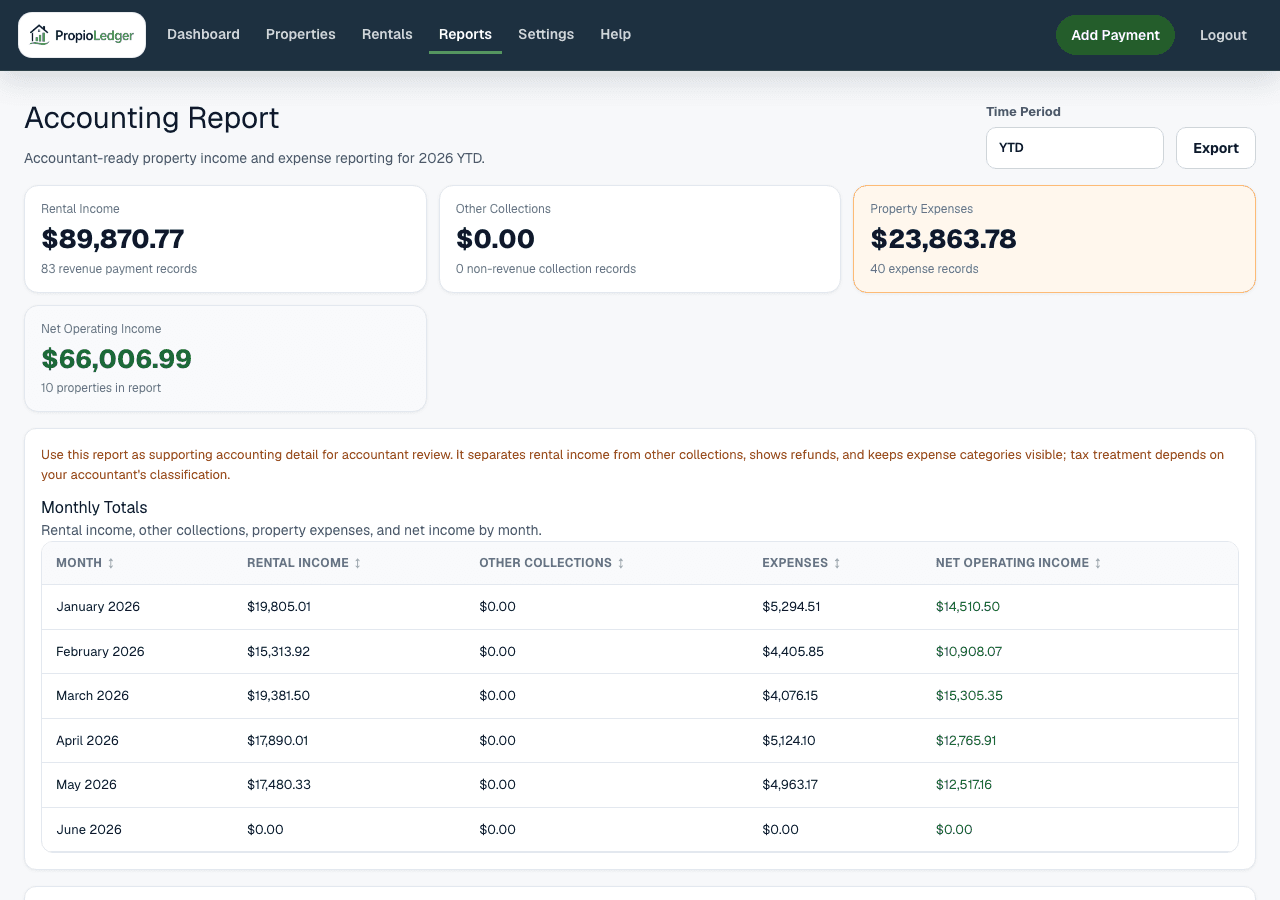

Reports Landlords Should Review

A bookkeeping system is only useful if it turns transactions into reports you can actually use. For small landlords, the most helpful reports usually answer a few plain questions: What came in, what went out, what is owed, and which properties are performing best?

In PropioLedger, landlords can review accounting reports, cash flow reports, expense analysis, property profitability, rental ledgers, open balance reports, past-due reports, revenue reports, and income forecasts. These reports are built from recorded activity, so the quality of the report depends on the quality of the bookkeeping.

- Accounting Report: rental income, other collections, property expenses, and net operating income for accounting review.

- Rental Ledger: charges, payments, credits, refunds, and running balances for renter account activity.

- Cash Flow Report: payment income, property expenses, and net cashflow by month and property.

- Property Profitability Report: income, expenses, net operating income, and net cashflow by property.

- Open Balance and Past Due Reports: unpaid visible charges and charges whose due dates have arrived.

- Expense Analysis Report: expenses by category, trend, and property detail.

Spreadsheet vs. Rental Bookkeeping Software

Spreadsheets are not wrong. Many landlords start there because spreadsheets are flexible, familiar, and inexpensive. For a single property with a small number of transactions, a well-maintained spreadsheet may be enough.

As portfolios grow, spreadsheets often require more custom tabs, formulas, manual links, and version control. Rental-focused software can help by giving income, expenses, payments, balances, and reports a consistent structure by property.

| Consideration | Spreadsheet | Rental-Focused Software |

|---|---|---|

| Initial setup | Flexible but manual | Structured workflow |

| Multiple properties | Requires custom tabs and formulas | Organized by property |

| Tenant balances | Must be built manually | Can be integrated with the rental ledger |

| Reporting | Requires formulas and upkeep | Generated from recorded activity |

| Error risk | Formulas and rows can break | More consistent data structure |

| Cost | Often low or free | Subscription cost may apply |

Related Guides

Rental Property Accounting Software vs SpreadsheetsCommon Rental Bookkeeping Mistakes

Most bookkeeping problems come from small habits repeated over time. The good news is that each mistake has a practical fix.

| Mistake | How To Avoid It |

|---|---|

| Mixing personal and rental transactions | Keep rental activity clearly separate and label owner contributions or draws. |

| Failing to assign expenses to a property | Require a property on every property-related expense. |

| Treating mortgage principal as an operating expense | Use Mortgage Principal for known principal amounts so it remains visible without reducing operating income. |

| Recording refundable deposits as rent | Track refundable security deposits separately from earned rental revenue. |

| Using inconsistent expense categories | Keep category names stable from month to month. |

| Combining repairs with improvements | Review significant projects and separate repairs from capital improvements. |

| Ignoring small recurring expenses | Record software, bank fees, utilities, and subscriptions before they disappear into statements. |

| Waiting until year-end | Review books monthly while details are still fresh. |

| Failing to review tenant balances | Use the rental ledger to keep open balances and past-due charges visible. |

| Relying on a single portfolio total | Compare income, expenses, cash flow, and profitability by property. |

Example: One Month Of Bookkeeping

Here is a simple example for Oak Street Duplex. The point is not that every property should look like this. The point is to show how one month of activity becomes useful when each item is classified clearly.

In this example, total rent collected is $3,200. Operating expenses shown here are $470 for the plumbing repair, lawn service, and insurance. The mortgage statement also shows $1,300 of interest and $600 of principal.

If you look only at cash leaving the bank, the month includes $2,370 of cash outflow. Mortgage Principal remains visible as part of cash flow, but it is not treated as an operating expense. This is why cash flow, accounting profit, and taxable income are not always identical.

| Transaction | Amount | Classification |

|---|---|---|

| Unit A rent | $1,650 | Rental income |

| Unit B rent | $1,550 | Rental income |

| Plumbing repair | $185 | Repairs |

| Lawn service | $120 | Maintenance |

| Insurance | $165 | Insurance |

| Mortgage interest | $1,300 | Mortgage Interest |

| Mortgage principal | $600 | Mortgage Principal |

Bookkeeping vs. Rental Property Accounting

Bookkeeping records transactions, organizes income and expenses, and maintains the financial history. Accounting uses those records to analyze performance, prepare reports, support tax work, and make financial decisions.

For a small landlord, the two ideas overlap in everyday work. You record the expense, assign it to a property, choose a category, and later review reports. The important thing is that accounting is only as useful as the bookkeeping underneath it.

Related Guides

Rental Property Accounting GuideA Simpler Way To Organize Rental Property Finances

A practical rental property bookkeeping system does not need to be complicated. It needs to be consistent, property-level, and complete enough that every transaction makes sense later.

PropioLedger helps small landlords track income, expenses, payments, balances, cash flow, and profitability by property. Instead of maintaining disconnected spreadsheets, landlords can keep their rental activity organized in one purpose-built system while still working with a qualified tax or accounting professional when needed.

Ready to Organize Your Rental Property Finances?

PropioLedger helps landlords track income, expenses, payments, balances, reports, and property performance without rebuilding records from disconnected spreadsheets.

Educational Disclaimer

This guide is for general educational purposes and is not tax, accounting, legal, or financial advice. Landlords should consult a qualified professional for guidance specific to their situation.